Last Updated on by Edward Harris

Affordable health insurance plans for the self employed are available. Regardless whether you need coverage for just yourself and your family, or a small business, low-cost policies can be easily purchased. Pre-existing conditions are covered, and a federal tax subsidy can substantially reduce your premium (if you meet eligibility requirements). The ACA Legislation provides assistance to freelancers that work for themselves, and are responsible for paying their own medical plan premiums. Entrepreneurs and persons that run their own business have access to a wide range of flexible plan options.

A sole Proprietorship is very common (millions of persons in the US) and many types of healthcare benefits are widely available. Whether you have no employees, a solo business, or 20 persons working for you, you still must purchase coverage, although small business requirements were temporarily postponed. Part of our expertise (more than 40 years of experience) is finding the new plans that will cost you the least, but still provide "essential" benefits. NOTE: If you own or operate a business with no employees, the Department of Health and Human Services classifies you as "self-employed." Many local and federal programs are available to offer medical coverage.

HSA Plans

HSA plans should always be considered, since they offer a choice of several deductibles, tax-favored deposits to pay qualified expenses, and lower premiums. Several deductible options are offered, and deposited funds can be invested conservatively or aggressively. All family members are covered and negotiated network discounts can save a substantial amount of money. Dental, hearing, and vision expenses can also be paid with tax-deductible deposits.

Funds that are not utilized for the calendar year will not be lost, and each year additional deposits can be made. Fixed accounts pay a modest amount of interest and the monthly maintenance fee is low. Although interest rates have reduced for 2026, the current rate is still substantially higher than five years ago. More aggressive equity options are also offered.

Medicare-eligible persons can also continue to use past accumulated funds for specific HSA expenses, but tax-deductible deposits will no longer be accepted. There is no penalty for withdrawing funds, but taxes may apply. Examples of covered items include nursing home expenses, protective health screenings, and non-conventional treatment for terminal illnesses. Higher interest rates paid on accumulated funds have also helped balances grow throughout the year. Long-time depositors can create a substantial accumulation for retirement years.

Once enrolled in Medicare, many medical out-of-pocket expenses (that have not been previously reimbursed) can be reimbursed. Common example include diabetic and insulin supplies, prescription drugs, over-the-counter drugs, coinsurance, copays, vision and dental expenses, and deductibles. Insurance premiums (Advantage, prescription drug, and supplemental) may also be able to be reimbursed.

The current 2026 HSA contribution limit is $4,400 for individuals and $8,750 for a family (increase from $4,100 and $8,300 two years ago). The minimum policy deductible is $1,700 ($3,400 per family). HSA-owners over age 55 can contribute an extra $1,000 per year (Catch-up contribution). An HDHP (High Deductible Health Plan) must be utilized to take advantage of the tax-deductible contributions. Generally, these options are are available in the Bronze and Silver Tiers. Coinsurance levels are typically 0%, 20%, 30%, and 50%. Note: HDHP maximum out-of-pocket amounts are $8,500 and $17,000. Last year's amounts were $8,300 (individual) and $16,600 (family). The deadline for making contributions is typically the federal income tax-filing deadline.

Advantages Of Working For Yourself

A major advantage of working for yourself (as opposed to owning a small business) is that you are eligible for potentially large federal tax subsidies to help pay your (and your family) medical insurance premiums. Since this assistance is in the form of an instant tax-credit, you don't have to wait months to receive the money, and your healthcare premiums can immediately reduce. This allows you to afford lower deductibles and smaller out-of-pocket expenses. Silver-tier plans utilize "cost-sharing for households that meet lower income requirements. Also available is a self-employed health insurance deduction on 100% of premiums.

If you leave your job, lose your employer-based coverage, and become self-employed, you will probably qualify for a Special Enrollment Period (SEP). This allows you to apply and enroll without answering medical questions. Other SEP exceptions are divorce, marriage, reaching age 26, becoming ineligible for Medicaid, and moving to a different service area. Typically, up to 60 days is granted to apply and enroll in a Marketplace plan offered by carriers in your area. You may also choose a non-Obamacare plan, although pre-existing conditions may not be covered, and all "essential benefits" may not be covered. An application fee may also be required.

Avoidance of the "SHOP" (Small Business Health Options Program) Exchanges (see below) saves time, money, confusion, and simplifies the process of comparing, choosing and enrolling for a plan. However, SHOP has certain advantages, including no Open Enrollment deadlines, and provider networks are generally quite robust. And since plans are offered throughout the year, coverage can be obtained very quickly, without waiting until January 1. The tax credit is the most generous to companies with less than 10 workers and if the average annual compensation is less than $25,000.

To obtain the credit, you must purchase a SHOP plan. The company also must have 1-50 full-time workers and offer benefits to all employees working about 30 weekly hours. 70% of the employees offered coverage must be enrolled. A "Minimum Participation Rate Calculator" can determine the exact number of workers that must enroll. If minimum participation requirements are not met, an Open Enrollment period takes place from November 15 to January 15.

SHOP is also viable option if you want to choose the amount you pay towards worker's premiums. Non-profit entities are eligible and enrollment takes place throughout the year (unlike the Marketplace). Employees can also enroll online and pay premiums on their coverage. As the owner of the company, you choose the percentage of worker costs that you pay. The credit is offered for a maximum of two consecutive years and IRS form 8941 must be completed.

If you have no employees, you can not utilize this program. However, you may be eligible to purchase a subsidized Marketplace plan. Persons who own and operate their business, along with self-employed persons and freelancers, can typically apply for Exchange plan coverage. Unless there is an approved qualifying event, you must apply during the Open Enrollment period. If the OE deadline is missed, alternative non-ACA options are offered. However, temporary plans are no longer a popular option due to the maximum four-month benefit period.

Premium Tax Credit Examples

The available credits are instantly applied to premiums. However, depending on the total Modified Adjusted Gross Income (MAGI), the amount of the subsidy could pay most or all of the cost of coverage, or pay a very small or perhaps no part of the rate. The relationship of the household income to the Federal Poverty Limit guidelines will determine the amount of the subsidy. Higher-income households will have to pay the full retail cost of Marketplace plans, or select non-Obamacare options that cost less, but omit several key provisions.

Shown below are several examples of estimated credits derived from the total household income. Amounts shown are monthly and can be instantly deducted from the premium. The subsidy is NOT taxable to self-employed persons or small business owners. Also, the subsidy is based on the projected current year's household income, and not last year's income. Note: It is possible that children in a household may qualify for CHIP benefits.

25 year-old in Jefferson County, CO. Household income is $30,000. Federal subsidy is $294.

25 year-old married couple in Jefferson County, CO. Household income is $50,000. Federal subsidy is $529.

30 year-old in Harris County, Texas. Household income is $25,000. Federal subsidy is $436.

30 year-old married couple in Harris County, Texas. Household income is $45,000. Federal subsidy is $793.

35 year-old in Franklin County, Ohio. Household income is $30,000. Federal subsidy is $401.

35 year-old married couple in Franklin County, Ohio. Household income is $60,000. Federal subsidy is $614.

40 year-old in Chatham County, Georgia. Household income is $32,000. Federal subsidy is $447.

55 year-old in Chatham County, Georgia. Household income is $40,000. Federal subsidy is $743

45 year-old in Salt Lake County, Utah. Household income is $55,000. Federal subsidy is $241.

35 year-old married couple in Salt Lake County, Utah. Household income is $72,000. Federal subsidy is $501.

40 year-old married couple in Putnam County, Indiana. Household income is $40,000. Federal subsidy is $687.

50 year-old married couple in Putnam County, Indiana. Household income is $72,000. Federal subsidy is $606.

55 year-old married couple in Dauphin County, Pa. Household income is $70,000. Federal subsidy is $1,999.

60 year-old married couple in Dauphin County, Pa. Household income is $70,000. Federal subsidy is $2,523.

Tax Ramifications Of Subsidy

It's important to understand that any Obamacare subsidy you receive is not considered taxable income. There is no 1099 federal tax form that will be issued as a result of your premium reductions. These credits are best used to immediately offset healthcare premiums although you can wait until you file your federal return (which we don't recommend). Also, you do not have to utilize the entire credit. If you choose a lower amount than you are entitled to, when you file your federal tax return the following year, you will receive the difference.

"Dollar caps" limit the owed repayment, unless your family income is four times the FPL (Federal Poverty Level) or higher. For example, If the household income is less than 200% of the FPL, the maximum taxpayer repayment is $375 ($750 per family). The maximum taxpayer repayment increases to $1,575 and $3,150 when the FPL is 300% to 399%.

Conversely, if you overestimate your income, you may be entitled to a refund. Rebate reimbursements from insurers (if they did not meet the requirements to limit expenses) may also generate a taxable event. That reimbursement may have to be reported as taxable income in the year you receive it. However, beginning five years ago, rebates were not reported by any of the carriers. Additional information is provided by the Self-Employed Individuals Tax Center, which reviews many issues including opening and closing a business, paying taxes, and the home office deduction.

NOTE: If you receive a subsidy, you are required to complete IRS Form 8962 (Premium Tax Credit) the following year. This form will generate a refund if you didn't use the entire credit, and will also deduct any over-payments you received as a result of underestimating your household income. It's extremely important to update your projected household earnings each year. Changes in employment or the number of household members can impact the amount of the subsidy. Any person that becomes eligible for Medicare or Medicaid is no longer eligible for tax credits. However, it is possible to qualify for a subsidy with dependents in the household also qualifying for CHIP benefits.

Some of the information needed to complete IRS Form 8962 includes total family size, modified MAGI, household income, federal poverty line (table provided), annual contribution amount, excess advance payment of PTC, and repayment limitation. Instructions for completing the form are offered.

What Is The Cheapest Plan?

Affordable Business-Owner Healthcare Is Available

Important components of the ACA legislation are "Metal" plans. All policies are placed into four categories: Platinum, Gold, Silver and Bronze. Platinum plans are the most costly policy since they are expected to cover 90% of projected medical expenses. The cheapest policy is the Bronze plan, which is expected to cover approximately 60% of projected medical expenses. Often, net premiums become $0 for Bronze-tier plans, although maximum out-of-pocket costs may still be $9,450 (individual) or $18,900 (family). See additional details below.

A special "Catastrophic" tier is provided for persons under age 30. However, federal subsidies are not applicable to this tier, and specialist visits and non-generic prescriptions are often subject to large deductibles. Also, in many situations, a Silver-tier or Bronze-tier plan is more cost-efficient, since specialist and urgent care visits may be subject to copays, instead of the policy deductible. Tier 2 and Tier 3 drugs also may not be subject to a deductible. Tier 5 specialty drugs are the most expensive prescriptions, and are subject to coinsurance and a deductible.

The maximum out-of-pocket expense for an individual in 2024 is $9,450 per year, which increased from $8,700 two years ago. The family maximum is $18,900. For QHDHP (Qualified High Deductible Health Plan) plans, the maximums are $7,500, and $15,000. Maximum annual HSA contributions are $4,150 for single plans, and $8,300 for family coverage. Non-grandfathered contracts must adhere to these guidelines. However, policies that are grandfathered (issued before April of 2010) do not have to meet these guidelines, if still in-force. Most grandfathered contracts are no longer active

Open Enrollment

Of course, your actual expenses could be substantially less, if there are no major medical claims and/or a relatively low number of symptomatic claims such as colds, the flu, and viruses. If you or a family member develops a serious chronic illness, you can switch to a different plan with lower out-of-pocket expenses (Gold, for example) during Open Enrollment each year. For 2023, the OE period began on November 1st, although the dates can change each year. NOTE: Medigap Open Enrollment typically begins earlier than OE for persons under age 65. The first day of enrollment was October 15th (Seniors). The first day of enrollment for applicants under age 65 is November 1.

Seniors who reach age 65 also have a seven-month window to select a Medigap plan. There is no obligation to select a plan and many consumers are provided benefits through a prior employer. Medicare/Medicaid options are available, if needed. It is possible that one spouse will qualify for Medicare, while another spouse qualifies for Marketplace coverage. A subsidy will still be offered although the entire household income must be considered, including social security and pension benefits. Applicants between the ages of 60 and 64 can qualify for large subsidies, especially if a spouse is also between those ages.

All preventive benefits for you or any other person named on the Bronze-type (and all others) policy are covered at 100%. For example, annual physicals, mammograms, children's well check exams and adult PAP tests will have no out of pocket expense to you. For females, cervical cancer screening is covered along with contraception, well-woman visits and osteoporosis testing (if over age 60). Thus, if you had no medical issues and were mainly concerned with catastrophic and preventative features only, the Bronze option (along with Silver-tier contracts) should be considered.

Many of the Exchange plans are HSA-eligible, which allows you to take advantage of tax-deductions for qualified medical, dental and vision expenditures. We wrote about the best available HSA plans, and endorse this type of coverage if you are concerned with reducing your premium while maintaining prominent benefits. If a serious chronic condition develops, you can change to a more cost-effective option effective January 1. When you become eligible for Medicare, although you can not make tax-deductible deposits into the account, you can use accumulated funds to pay out-of-pocket expenses.

Will The Government Help The Self-Employed?

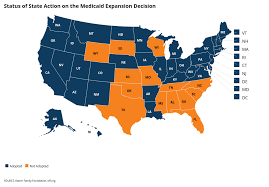

Yes. For example, if your income is below 133% of the Federal Poverty Level (FPL), you may be eligible for Medicaid, which will pay for most/all of your healthcare expenses. Each state has the choice of expanding Medicaid eligibility (from the current 100% of FPL) and the map below (provided by the Kaiser Foundation) provides a current status. As of 2023, 40 states had expanded Medicaid with a few more states actively discussing the possibility. "Medicare-For-All" is generally a hot topic during Presidential elections, but appears not popular enough to be passed in Congress.

State Medicaid Expansion (Updated 2020)

Even if you're not considered "low income," the government can still help. Also, you are no longer taxed ($695 per person/ $347.50 per child, or 2.5% of your income, whichever is greater), if qualified coverage is not purchased. Non-compliant plans can be purchased with no additional tax. Previously, if you secured a policy during the year, the penalty was pro-rated. $2,085 was the maximum penalty for a family, and generally, the first three months of not having coverage, were not counted in the tax. Although the non-compliance penalty has been eliminated, millions of Americans continue to qualify for low-cost healthcare...but don't take advantage of the opportunity.

In the following scenarios, we have illustrated the significant reduction in premiums you may qualify for. We assumed a household with a husband, wife, (ages 35-50) and one child, residing in Franklin County in Columbus, Ohio. Costs and subsidies shown are monthly amounts. The subsidy can be instantly deducted from premium, and the least-expensive Bronze-tier plan was chosen.

Age Income Healthcare Cost Federal Subsidy

35 $60,000 $798 $810

45 $70,000 $891 $818

45 $80,000 $891 $695

48 $90,000 $985 $676

48 $95,000 $985 $623

In all of the scenarios, a substantial amount of the health insurance premium is paid by the federal subsidy, including a whopping amount for the 45 year-old (and family) with $70,000 of family income. Naturally, the older you are and the less money you make, the greater your subsidy. Also, households with children that are listed as dependents on your federal tax return will also qualify for much higher subsidies. NOTE: In these examples, adding a second child would result in Medicaid (CHIP) eligibility for the children, and lower the premium and subsidy. The cost of Medicaid benefits are extremely low, although the number of available Network providers will be less than what is offered through a large carrier. CHIP benefits are very comprehensive, and feature low premiums for young dependent children.

It's also important to understand that we based these projections on the purchase of the cheapest available "Silver" plan. This specific policy is designed to pay an estimated 70% of your anticipated medical expenses. Thus, if $3,000 is the average amount of expected expenses, your portion would be $900. Of course, your out-of-pocket cost could be substantially less if you have a healthy year. Your copay for specialists, the ER, and Urgent Care facilities can greatly impact your potential out-of-pocket expenses. Also, carriers often exit and re-enter specific state markets. It is possible your plan may no longer be offered at the Jan 1 effective date. If this occurs, typically, you are provided 60-120 days before the termination date (or earlier).

Silver plans are also one of the most offered options, since companies must include this type of policy in their portfolio if they are participating in the Exchange. They are also considered "benchmark" plans since the amount of the initial federal subsidy is often calculated on on Silver options, regardless if you chose a Platinum, Gold or Bronze plan. However, benefits (other than deductibles/copays) are the same for the four Metal plans. Out-of-pocket costs can vary greatly for Tier 3, 4, and 5 prescription drugs.

Silver-tier plans are priced to pay approximately 70% of the expected medical expenses for all family members. The remaining balance is paid through copays, coinsurance, deductibles, and maximum out-of-pocket expenses. Naturally, extremely healthy enrollees will pay much lower amounts. Federal regulations, however, allow insurers to allow the actuarial value on these plans to fluctuate between 66% and 72%. Services that are performed with out-of-network providers are not counted.

Key Fact: If the household income is less than 250% of the Federal Poverty Level (FPL), special "cost-sharing" can be applied to the policy. This feature (unique to Silver-tier) can reduce a deductible by thousands of dollars and potentially save $5,000 per year (or more). If you qualify for this option, all Silver-tier contracts should be considered. In many situations, they will provide lower premiums AND lower out-of-pocket costs than Gold-tier plans. For self-employed persons, the savings from lower copays, deductibles, and maximum out-of-pocket expenses can be thousands of dollars each year.

If You Are Young And Healthy, A Cheap Catastrophic Plan Should Be Considered

Young, Healthy, And Self-Employed?

A special and envious situation is if you own your own successful business, and you're young and healthy. Do you really need medical coverage? Although the likelihood of utilizing the coverage is fairly low, the risk still exists that a major illness or disease could cost thousands of dollars (or hundreds of thousands). This is not a risk that you should take lightly, even though the 2.5% non-compliance tax has been eliminated. If you miss the Open Enrollment deadline, a short-term plan should be purchased to provide coverage the remainder of the calendar year. The cost is low and major medical benefits can be provided.

Securing basic major medical coverage is critical, even if it results in purchasing a 12-month short-term plan (non-compliant). The alternative of having no coverage can result in tremendous financial obligations that will have to be paid over an extremely long time. Health coverage for the self-employed is less expensive than most persons realize. Although most temporary plans exclude pre-existing conditions from being covered, large expenses are part of the benefit package.

An affordable and popular solution is to consider purchasing an "off-Exchange" policy from one of the major companies. Although you will not receive a subsidy, it is not a concern since you may not be eligible because of your high income. Selecting a high-deductible plan will provide cheap catastrophic benefits from a reputable and reliable company, and preserve your estate and assets if you were to incur tens (or hundreds) of thousands of dollars of medical bills. In many states, selected carriers offer non-subsidized plans, but not Marketplace plans. Often, carriers offer non-Exchange options that are not offered through the Marketplace.

My Spouse Has Benefits At Work

If your wife or husband has healthcare benefits from their employer, coverage may be offered to you, regardless of your employment status (retired, self-employed, or working for an employer). Marketplace plans are always available, but a federal subsidy will probably not be offered, based on current guidelines. Group spousal coverage is sometimes very expensive compared to the primary employee's cost. Dependent coverage may also be quite expensive although off-Exchange options can be considered for persons with no pre-existing conditions.

Under ACA legislation, companies with more than 49 employees must offer healthcare benefits to their workers, and any child that has not reached age 26. They are not required to offer medical plans to spouses of employees. However, the majority of employers offer coverage options if the spouse is not eligible for coverage through their existing employer. If minimum value and affordability tests are not met, a subsidy would become eligible for Exchange plans. This often results in much lower premium than selecting the group plan option.

An LLC May Allow You To Tax-Deduct Health Insurance Costs

A limited liability company (LLC) is a company that is created so the owner (or owners) are not liable for the company's obligations, liabilities, or debt. Considered "pass-through entities, the owners file their own tax returns. Pass-through taxation and legal liability are the backbone of an LLC. These setups are also used with a sole proprietorship or partnership. Legal liability is also separated from the owner. Thus, if a lawsuit is filed against the LLC, the owner's assets are not at risk.

An LLC is allowed to deduct the cost of medical benefits for workers that are not part of the LLC. Long-term care coverage, if included in premiums, is also deductible. If you are self-employed, deduction of medical, long-term care, and dental coverage is permitted for yourself and other immediate family members. The AGI (Adjusted Gross Income) reduces, which provides some insulation against future phase-out legislation.

A sole proprietor can qualify for a single or family Exchange plan with subsidies. A group insurance plan will probably not be an option if there are no employees. Just one employee is required to obtain group benefits with most carriers. If there are no employees, a Marketplace plan can be purchased. A sloe proprietor with one employee (not counting the owner) can typically qualify for a group plan. If corporate tax treatment is received, generally, a member is not eligible for medical benefits unless they are actual employees.

Cheap health insurance for the self-employed can still be found. We shop all of the available options so you can spend less time worrying about your medical benefits, and can concentrate on growing your business and enjoying your free time. If you hire part-time or full-time employees, we assist in finding your workers affordable medical benefits. Small group plans are offered by most major companies with very flexible coverage options.

PAST UPDATES:

As you prepare to file your federal tax return, if you enrolled in an Exchange plan, you'll need an additional form this year -- the 1095-A, which is the Health Insurance Marketplace Supplement. The expected arrival date is before February 1, and your return can not be processed without it. Copies can be downloaded online or picked up at any IRS office.

This new form provides information regarding the premiums you paid throughout the year and the federal subsidies you received that were credited towards the payments. Since the same information is reported to the Internal Revenue Service, it's important that the information you provide is identical to IRS documents. There is a publication (#5187) that helps explain some of the process.

Rates will be published shortly. Although prices will be increasing on the majority of plans in all states, the projected hikes are typically 3%-8%. However, there are several notable exceptions of 20%-35%. There is good news for self-employed households since popular HSA plan rates are not expected to substantially increase. In many states, there is little or no change from last year's pricing. However, maximum contribution amounts and minimum allowed deductibles are changing.

Despite several recent tax code changes, health insurance premiums still may be able to be deducted on line 29 of Form 1040. However, your business must be profitable on Schedule C.

Business owners and self-employed professionals may need to prepare for sharp rate hikes in future years. Although prices are not yet published, in many areas, increases of 10%-20% are expected for healthcare premiums. Increasing the deductible and out-of-pocket cost maximums can help lessen the increases. Also, if Congress can agree on a plan to either tweak or change the Affordable Care Act legislation, 2027 numbers may be more favorable.