Get cheap health insurance rates by easily comparing the best private and Marketplace prices in your area. Review all available plans and search for doctors, hospitals, and covered prescription drugs. You're just minutes away from finding the most affordable medical plans for individuals, families, the self employed, Seniors, and small business owners. The online quotes we provide are free, and our 40 years of unbiased recommendations, expertise and experience ensure you receive the best prices and you will be able to easily shop and enroll online.

You can always view options from multiple companies in your area 24/7, and many low-cost budget options are offered. Short-term, student, business, and Senior Medigap plans are also available with PPO, HMO,and EPO networks. Non-Obamacare options are offered at all times throughout the year, including inexpensive short-term temporary coverage. Medicare plans are offered for persons age 65 and above, including Supplement, Part D prescription drug, and Advantage options. Senior coverage also covers pre-existing conditions and has a specific Open Enrollment period.

During Open Enrollment, 2024 subsidized plans are available from top-rated companies along with Medicaid/Chip options, depending on your household income and size. Both before and after Open Enrollment, special exceptions are offered if you lose qualified coverage, have a baby, move to a different area, get divorced, or qualify for many other situations. You can also obtain affordable coverage "outside" of the Marketplace, where the number of available network providers (doctors, specialists, hospitals, Urgent-Care, and other facilities) is often larger. Policies are offered for every budget, and with each enrollment, you may keep an existing plan or select a new option.

Note: Newborns can obtain guaranteed coverage at any time of the year, regardless of any existing conditions or pending surgery. A "special life event" allows you to qualify for an SEP. Immunizations and well-visits are covered, along with any type of juvenile sickness or illness. A newborn can also be covered under a parent's Group policy provided by their employer. COBRA, if available, provides coverage for adults and children. Although prices are high, pre-existing conditions are covered and benefits match the coverage you had through the employer. Dental, hearing, and vision benefits can typically be retained.

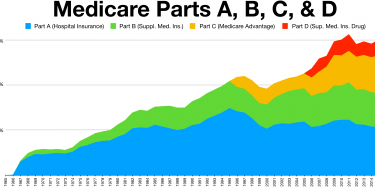

Senior Medicare Coverage

2024 Senior Medigap contracts from many companies are also easily reviewed. Benefits and price can vary, depending upon age, gender, county of residency, coverage, and plan availability. Although typically prescription drug Part D plans are offered statewide by participating carriers, Supplement and Advantage plan availability can vary in different counties. Advantage plans often cost less a Supplement policy, the provider network must always be considered.

Coverage is also offered to persons that are eligible for both Medicaid and Medicare (Dual Plans). Typically dual eligibility results in the majority of your health care expenses being covered. Medicare is the primary carrier and initially pays covered expenses. Supplement and employer group plans pay next. Several states include prescription drug benefits in these types of plans.

We understand that each applicant has different healthcare requirements, largely depending upon what medical conditions (if any) they are being treated for. Since every insurer now underwrites policies according to more consumer-friendly guidelines (non-medical), we shop all of the large reputable companies so you will be matched with the best available offers. Of course, other factors can impact premiums such as where you live, your age, household income, plan availability in your county, and the type of benefits you need.

Also, as later discussed, your income will determine the eligibility and level of federal subsidy you receive to help pay premiums on under-65 health insurance policies. But you will not be denied a policy because of existing conditions, such as diabetes, cancer, rheumatoid arthritis, or heart disease. On the policy effective date, full benefits will begin without a reduction in coverage or waiting period because of an existing condition.

Medigap plans are available when you reach age 65 and are eligible for Medicare. A separate enrollment period is also offered from October 15th through December 7th, with Supplement, Advantage, and Part D drug prescription plans offered. You can coordinate your standard benefits with a supplemental plan that will pay many out-of-pocket expenses, and perhaps include dental, vision, and hearing coverage. Plan G (HD) Supplement plans are typically the lest expensive MedSup option. The 2024 yearly deductible is $2,800, with 100% coverage thereafter. The Affordable Care Act and future Administration legislative changes generally do not greatly impact Medigap retiree options. However, Medicaid benefits, CHIP, and plans for persons under age 65 are typically affected.

Good Or Bad Health

If you are not in perfect health, or have conditions that require treatment and/or medications, low-cost plans may still be offered. Under the Affordable Care Act (ACA) legislation, your pre-existing conditions are covered, and do not impact the premium you pay or the benefits you receive. Marketplace plans are also eligible for an instant federal subsidy that can pay a substantial portion of your policy costs, and possibly the entire premium. Silver-tier plans feature "cost-sharing," which can substantially reduce out-of-pocket costs, including deductibles, coinsurance, and copays. Cost-sharing reductions (CSR) are offered to households with income up to 250% of the federal poverty limit. These amounts are not considered credits and do not have to be reconciled at the end of the year.

You may also find several plans that have a $0 net premium after the instant tax credit has been applied. The subsidy is based on your projected income for the upcoming year, and not your earnings from previous years. It is not taxable, and you can adjust the level, depending on current household income projections. If you become eligible for Medicare or Medicaid, the federal subsidy that other family members receive may be impacted. Adjustments can be made throughout the year to remain compliant.

Note: Senior Medicare Supplement plans are standardized, and are not eligible for the same federal aid that applicants under age 65 receive. Advantage plans offer consumers the opportunity to replace standard Medicare benefits with coverage provided by a private insurer. Often, prices of these plans are low, and several ancillary benefits are included, including dental, vision, and hearing coverage. Fitness Club memberships and several other perks are are also sometimes included. However, a specific network of providers must be utilized, and changing to a standard plan is allowed only during designated times.

Original Medicare plans allow all covered persons to select treatment with the vast majority of providers, including hospitals, specialists, and primary-care physicians. Most Supplement contracts also allow you to utilize any provider. "Medicare Assignment" is typically required for out-of-pocket costs to be paid, meaning that the negotiated prices must be accepted, and medical claims will be processed upon your behalf. Plan G (HD) offers lower premiums (see above), but a $2,800 deductible must be met before most expenses are paid.

Plan G (HD) is offered to applicants that became eligible for Medicare two years ago. Often, persons with no health problems choose this option since premiums are typically less than $60 per month. Although the Part B deductible is not paid, covered benefits include Part A coinsurance and hospital costs, Part B coinsurance, skilled nursing facility coinsurance, and Part A deductible. Insurers will waive out-of-pocket costs for countrywide conditions, such as the Coronavirus.

The more dependents in your household, the higher your financial aid becomes. In some states, the eligibility requirements for Medicaid have expanded, and more children are eligible for free or extremely low premiums. CHIP benefits are very comprehensive and it is possible for parents to qualify for conventional plans while their dependents qualify for Medicaid. Often, the combination of parents having Marketplace coverage, and their children covered through CHIP, creates a very cost-effective combination.

Higher-income households can find cost-saving Health Savings Accounts (HSAs) that allow deposits to pay for qualified medical, dental, and vision expenses. Many of these options are not found on the government healthcare website, since they are not subsidized by the federal government. Once an HSA owner becomes eligible for Medicare, accumulated funds can be used for qualified expenses. However, additional deposits can not be made.

Health Insurance Exchanges

The cost that you pay for coverage may change each year, depending on your renewal premium. The main factors that determine that premium, are where you live, your age, the size of your household, and whether you smoke. States like New York, New Jersey and Connecticut still cost more than Ohio, Indiana, Pennsylvania, and many other states in the Midwest. But several national and smaller regional companies offer policies in most parts of the country. The result has been more affordable and innovative private policy options. Examples of regional companies that offer competitive rates include:

Taro Health -- Maine

Piedmont Community Healthcare -- Virginia

Geisinger -- Pennsylvania

Wellmark Health Plan -- Iowa

QCA Health -- Arkansas

Meridian Health Plan -- Michigan

Priority Health -- Michigan

McLaren -- Michigan

Common Ground Healthcare Cooperative -- Wisconsin

Group Health Cooperative of South Central Wisconsin -- Wisconsin

Dean -- Wisconsin

Wisconsin Physicians Service -- Wisconsin

Neighborhood Health Plan Of Rhode Island -- Rhode Island

SummaCare -- Ohio

Denver Health -- Colorado

Montana Health Cooperative -- Montana

Florida Health Care Plan -- Florida

Vantage Health -- Louisiana

LifeWise Health Plan of Washington -- Washington

PacificSource -- Oregon, Idaho, Washington, and Montana

Sanford Health -- South Dakota and North Dakota

Moda -- Alaska, Washington, and Oregon

L.A. Care Health Plan -- California

Chinese Community Health Plan -- California

MVP Health Plan -- Vermont and New York

University Of Utah Health Plans -- Utah

Avera Health Plans -- South Dakota and Iowa

Sanford Health Plan -- Minnesota, Iowa, North Dakota, and South Dakota

Jefferson Health Plan -- Pennsylvania and New Jersey

The Exchanges

Each state utilizes the federal or their own "Exchange," where highly-rated insurers and occasional Co-operatives offer coverage. The number of plan options vary, depending on the state, and the approval time is typically streamlined. We guide you through the entire enrollment process so you easily find affordable medical coverage. Most State Exchanges are federally-run, since it is less expensive, and more government assistance is provided. Also, several state-run Marketplaces (such as Oregon) have resulted in the failure to properly enroll applicants safely and timely. The average cost of health insurance can vary greatly between states, and also counties within the same state.

Many companies are offering 2024 plans, although in several areas, only one company underwrites plans. Typically, Bronze, Silver, and Gold-tier plans are offered. In some areas, however, a carrier will not offer a catastrophic plan or a policy in the Platinum tier. Platinum policies have become very unpopular because of their high cost. They are also ineligible for cost-sharing, and often have high maximum out-of-pocket costs. Health applicants typically should not apply for Platinum-tier plans.

You can also purchase policies that are considered "off-Exchange." These plans contain all of the required "essential health benefits" and previously provided an exemption from paying a non-compliance tax. Major companies (Blue Cross Blue Shield, Aetna, UnitedHealthcare, Cigna, Kaiser, Humana and others) frequently offer these policies. Premiums are not eligible for subsidies, although the number of available network providers is generally equal than comparable Exchange contracts.

The enrollment process is also streamlined, and can often be completed in less than 10 minutes. Generally, HMO, PPO, and EPO network options are your provider-network choices. Many companies offer "tiered" networks, which provide lower copays and out-of-pocket expenses if you choose "preferred physicians and specialists. Western Pennsylvania's UPMC, for example, offers "Partner," "Select," and "Premium" options. Most carriers offer coverage in additional states, including nationwide networks.

The Marketplace application is short, but there are many confusing questions, including income and identity verification. Our experience and expert guidance speeds up the process so you can obtain coverage quicker, and avoid the glitches and delays that have impacted many persons. We not only help you find the right policy, but we assist you in the subsidy calculation that reduces your rate. If any family member is eligible for Medicare, Medicaid, CHIP, or any other federal or state program, we will review the specific details.

Seniors that are Medicare-eligible, can review supplemental plans and prescription drug plans (Part D) offered in your area. Advantage (MA) contracts will also offer low-premium options, although the provider network must be considered. MA plans may include dental, vision, and hearing benefits.

5-Star Medicare Advantage Plans

Community Blue HMO Medicare Prestige

Devoted GIVEBACK

Devoted PRIME

Devoted DUAL PLUS

Humana USAA Honor

Humana Gold Plus Lung

Humana Gold Plus -- Diabetes And Heart

Optimum Platinum Plan

Optimum Gold Rewards Plan

Security Blue HMO -- POS ValueRx

Security Blue HMO -- POS Basic

Security Blue HMO POS Standard

Security Blue HMO POS Deluxe

Select Health Medicare Flex

Select Health Medicare Essential

Select Health Medicare Dual

Simply More

Simply Extra

Simply More Platinum

Simply Level

Simply Level Platinum

UnitedHealthcare Care Advantage

UnitedHealthcare Nursing Home Plan

UPMC For Life PPO Rx Enhanced

UPMC For Life HMO Rx Enhanced

UPMC For Life HMO Deductible Rx

Regarding the previously-mentioned subsidy, it is applied in the form of an instant tax credit. You do not have to file a tax return to get it, and you won't have to copy a form and send it in the mail and wait six weeks either. It's instantaneous and is applied directly during the initial process. If you qualify for a federal subsidy, and subsequently use the credit to pay your premium, IRS Tax Form 8962 (Premium Tax Credit) should be filed to reconcile the amount. For example, if your income was less than originally projected, you will receive a refund for the premium over-payment. Form 1095-A will also be needed. If your household income substantially changes during the year, you can adjust your financial aid accordingly.

The Affordable Care Act legislation previously required you to buy health "qualified" insurance. Since it is no longer mandated, you are not assessed a tax penalty (2.5% of household income) if you don't comply with this "minimum essential coverage mandate". If you are covered through an employer-provided group plan, CHIP, Medicaid, or Medicare, incarcerated, or you are an undocumented immigrant, the penalty did not apply. The elimination of this part of the ACA Legislation has helped temporary 12-month plans become more popular. 24-month short-term options are also available in several states, although they may be expensive than shorter-duration contracts.

Most Affordable 2024 US Health Insurance Plans

Listed below are several of the most affordable healthcare plans available to individuals and families. Typically, these policies are not offered in all states.

Ambetter Standard Expanded Bronze

Ambetter Everyday Bronze

Ambetter Choice Bronze HSA

Ambetter Elite Bronze

Amerihealth IHC Bronze EPO HSA

Anthem Bronze Pathway Transition

Anthem Bronze Pathway X HMO 8700

Anthem Bronze Pathway X HMO 6000

Anthem Bronze Pathway X HMO 5000

Arkansas BCBS Bronze Plan 1

Ascension Personalized Care Balanced Bronze 2

BCBS Blue Local Bronze

BCBS BlueEssentials Bronze 1

Bright HealthCare Bronze 8700

Bright HealthCare Bronze 7200

Capital Blue Cross Bronze Capital Advantage EPO 7450/0/50

Capital Blue Cross Bronze QHDHP PPO 6300/0/50

CareSource Marketplace Bronze

Common Ground Healthcare Cooperative Value 1 Bronze

Fidelis Care Bronze

Friday Health Plans Bronze Basic

Friday Health Plans Bronze Plus

Highmark Together Blue EPO Bronze 3800

Highmark Together Blue EPO Bronze 6900 HSA

Kaiser Bronze 60 HDHP

Kaiser Signature Bronze 6500/40%/HSA

Kaiser Bronze 7500/40%/Vision

Kaiser Virtual Plus Bronze

Keystone HMO Bronze

L.A. Care Bronze 60 HMO

Medica Bronze Value

Medical Mutual Market HMO 8700

Medical Mutual Market HMO 8000

Moda Pioneer Bronze 8500

Oscar Bronze Simple

Oscar Bronze Super Simple

Oscar Bronze Classic

Providence Health Plan Connect 8700 Bronze

SelectHealth Signature Benchmark Bronze 8700

UnitedHealthcare Bronze Essential+

UPMC Advantage Bronze $6700/$0

Vantage Bronze Savings 7050

Wellmark Bronze HDHP HMO

Wellmark Bronze Modified HMO

Example Of Tax Credit That Helps Reduce Healthcare Premiums

Here's a quick example: Assume you and your spouse are 55 years old and you have two children in the household. You reside in Peoria County (Illinois) and your approximate household income is $105,000. Since you are not eligible for a subsidy, the unsubsidized monthly premium of the least expensive plans cost $1,862 (BCBS Blue Precision Bronze HMO 205) and $2,150 (Health Alliance POS HSA 6750 Elite Bronze). The least expensive Silver-tier plan (Blue Precision Silver HMO 206) costs $2,305 per month.

However, if the household income is only $90,000, the monthly premium of the BCBS Blue Precision Bronze HMO 205 option plummets to $5, with the help of a subsidy worth more than $23,000 per year. The cost of the Blue Precision Silver HMO 206 plan reduces to $309 per month. The qualification of federal assistance has a huge impact on the price you pay. But if your income changes, it is imperative to recalculate your subsidy to avoid a massive tax bill. Conversely, a substantial reduction in income could also lower your premium by hundreds of dollars each month.

Naturally, there are many different scenarios involving four different plan options (Bronze, Silver, Gold and Platinum). The least expensive plan (Bronze) has higher potential costs if you have a large claim, while a Platinum-tier policy will minimize your deductibles, copays, and coinsurance, but also raise the premium. Often, the "sweet spot" of coverage is a plan with moderate office visit copays ($30 for pcp and $60 for specialists) and a mid-range deductible ($3500-$5,000). For healthy families with multiple children, a combination of high deductibles ($5,000-$8,700) and lower office visit copays ($10-$25) can be very cost-effective.

We help you review and understand all options in your area, subsidies, tax breaks, and how it impacts the price you pay for your medical coverage. Any changes implemented by the current Administration are also reviewed, so you can take advantage of more flexible options. We also do what we do best. And that's find the lowest health insurance Exchange prices in your area. The Marketplace was created to provide subsidized plans for low and middle-income consumers. For upper-income households, affordable policies are also offered.